Academic

with Johannes Stroebel and Julian Terstegge

R&R at the Journal of Financial Economics

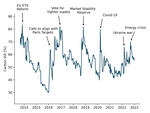

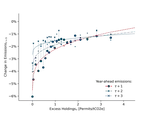

We study the effects of carbon price uncertainty on firms’ decisions to decarbonize their operations. We first use information on option prices for emissions allowances in the European Emissions Trading system to create the Carbon VIX, a market-based high-frequency measure of carbon price uncertainty. We then construct a measure of expected aggregate decarbonization investments via stock returns of “carbon solution providers”. Consistent with real-option theory, we find a 10 percentage point increase in carbon price uncertainty has a similar negative impact on decarbonization activities as a EUR 11 decline in the carbon price.

Data available at: www.carbonvix.org